The population and the private sector have already begun to pay the price for the political crisis triggered by the PSD, through the withdrawal of ministers from the government on April 23. The cost of the crisis enters the real economy with a significant depreciation of the euro/lei exchange rate, which in just a few days was -2%.

The euro reaching 5.2 lei/unit is not the only effect, although it is the most powerful in terms of negative effects – leading directly to the increase in the prices of imports, services quoted in euros (loans, rents, certain bills such as phone bills, etc.).

But before the depreciation of the national currency, the shockwave of the first round's result was transmitted especially in Romania's financial economy: investors, both local and international, reacted to the political crisis and implicitly to the appearance of political instability by being active in the markets through selling local assets (government bonds and shares from the BVB, for example) and moving money to other countries or, in the case of the Romanian population, to euros and euro-denominated assets.

A Weaker Exchange Rate Pressures Public Debt, Half Denominated in Foreign Currency

The political crisis and even the depreciation of the exchange rate risk derailing the fiscal-budgetary adjustment process that the European Commission and rating agencies have been demanding from us, and which the Fiscal Council and the National Bank of Romania keep insisting on and for which the Bolojan Government has adopted a wide range of unpopular measures. In fact, the NBR pegged the exchange rate in recent years to support the adjustment, which, however, has been postponed for years by the authorities until the Bolojan Government, as the budget deficit reached a crisis level or severe recession in 2024: 9.3% of GDP.

Romania is at risk of practically entering a classic emerging market crisis (such as Argentina, for example, which does not have stability anchors like the EU and NATO), where a political crisis, coupled with large budget and current account deficits, leads to a loss of market and investor confidence and, implicitly, large capital outflows.

I. NBR Reserves Drop by Over 2 Billion Euros: Exchange Rate Pressure Leads to Costly Interventions

The foreign exchange reserves at the National Bank of Romania (NBR) stood at 64.83 billion euros on April 30, 2026, down by over 2 billion euros from 67 billion euros on March 31, 2026.

The decrease came in the context where the NBR most likely intervened in the foreign exchange market to curb exchange rate volatility. Overall, regarding the NBR's foreign exchange reserve, in April 2026 there were inflows of 1.8 billion euros, "representing the change in the minimum foreign exchange reserves held by credit institutions at the NBR; funding the Ministry of Finance's accounts, and others."

The outflows were 3.996 billion euros, "representing the change in the minimum foreign exchange reserves held by credit institutions at the NBR; payments of principal and interest on public debt denominated in foreign currency; payments from the European Commission's account, and others."

Overall, Romania's international reserves (currencies plus gold) on April 30, 2026 were 78.007 billion euros, compared to 80.278 billion euros on March 31, 2026. Regarding the maturing payments in May 2026 on public debt denominated in foreign currency, directly or guaranteed by the Ministry of Finance, these amount to approximately 1.417 billion euros.

The NBR seems to still be present in the market to counteract an aggressive depreciation surge, but the fact that the exchange rate has broken through the previously defended BNR threshold (5.1 lei/euro) and has gone directly to 5.2 lei/euro shows that the pressure on the exchange rate depreciation is strong - making intervention too costly in relation to possible benefits.

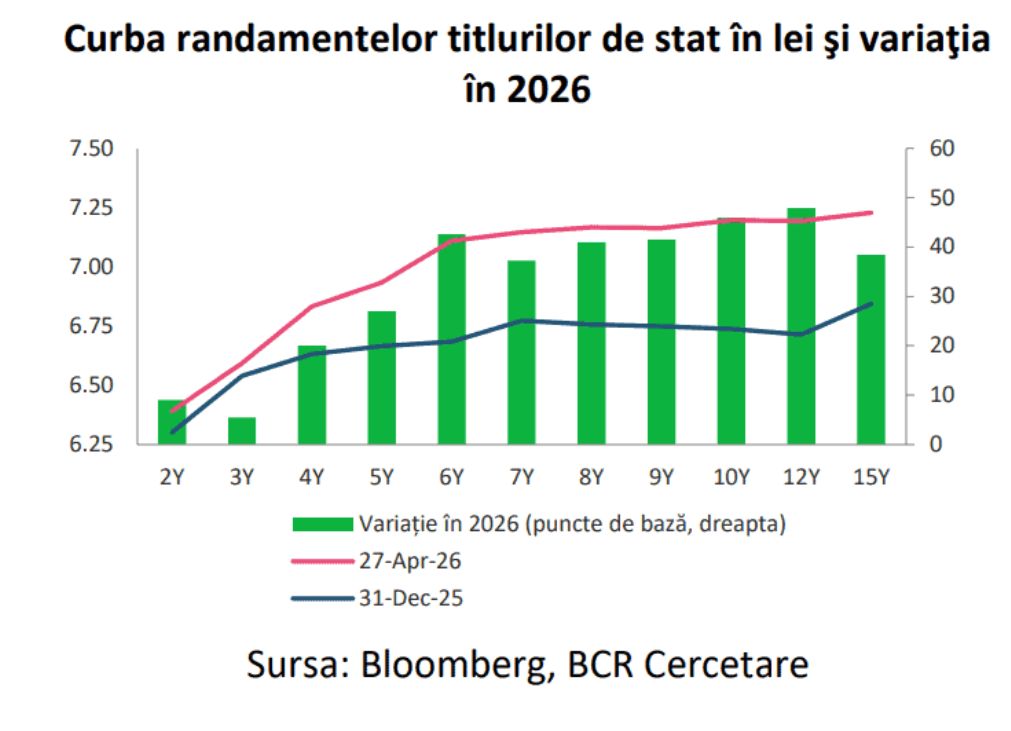

II. Only 2.62 Billion Lei Borrowed: Interest Rates Rise by 0.5 pp, Surpassing 7% in 5 Years

At the same time, the political crisis, overlaid with the war in Iran and the related energy crisis, completely disrupted the internal financing of the budget deficit and the need for funds to roll over the debt maturing this year.

In March, a month marked by uncertainty and major volatility in international and local financial markets, the Ministry of Finance raised only 1.8 billion lei from the local market (against a normal monthly average of over 10 billion lei).

At the same time, since the start of the political crisis initiated by the PSD on April 14-15, Finance has borrowed only 2.62 billion lei, well below the Treasury's regular program. Although the amounts are smaller, interest rates have increased significantly, by approximately 50 basis points (0.5%) across Romania's debt yield curve.

However, compared to the end of February, when the US started the war against Iran and interest rates had dropped to a two-year low, we are talking about an increase of approximately 100 basis points (1%) across the sovereign debt yield curve.

A 1 pp Increase in Interest Rates Adds Nearly 10 Billion Lei to Public Debt Servicing

It is worth noting that, before the onset of the political crisis, the 10-year bond yield had fallen to 6.69%, the lowest level since the beginning of the American-Israeli war in the Middle East (see graph above), which disrupted the downward trend from late 2025 and early 2026.

The entire yield curve (from short-term to long-term) had fallen well below the 7% threshold two months ago, before the Middle East war - Romania's yields had reached their lowest level in the past two years before the war, amid positive budget execution at the end of 2025 and early 2026.

The 1% decrease in the 10-year bond yield from late 2025 and early 2026 occurred at the cost of increased taxes, inflation at nearly double-digit levels, and a significant decline in consumption.

Regarding the impact of rising interest rates on public debt servicing, in the event of a 1 percentage point increase in interest rates and their remaining at the higher level, the Public Debt Management Strategy developed by the Ministry of Finance at the end of 2025 shows that this will lead to an increase in debt servicing payments by approximately 4.7 billion lei (0.8% of central government revenues) for debt in the national currency, and by approximately 5.0 billion lei (about 1.0% of central government revenues) for debt in foreign currency.

Read the full analysis Political Crisis, the Bill for the First 11 Days: 10 Billion Lei Extra from Public Debt Interest - a 2 Billion Euro Decrease in NBR Reserves to Prevent Exchange Rate Explosion - an Unknown Increase in Inflation due to Leu Depreciation on Curs de Guvernare